Following on from the first part of my June FOMC preview yesterday (here), this post looks at the likely changes to the statement, economic projections and interest rate ‘dot’ plot.

Now that the Fed are in more traditional data-dependency mode, I expect only the first paragraph of the statement to change, reflecting the data developments over the past 6 weeks. As ever, it is the adjectives that will determine whether it is taken hawkishly or dovishly. One possible addition to the statement (which I have not included below) is something that essentially says every meeting from here on is “live”. Yellen has said it in the past, but given the market is only focusing on press conference meetings (Sept, Dec) for first hike, the Committee may choose to be more explicit about moving outside those months. Here is my attempt at guessing how the opening para will change:

Information received since the Federal Open Market Committee met in

MarchApril suggests that economic growth has rebounded somewhatslowed during the winter months, in part reflecting transitory factors. The pace of job gains has picked upmoderated, and the unemployment rate has remained steady. A range of labor market indicators suggests that underutilization of labor resources diminished somewhatwas little changed. Growth in household spending rose modestlydeclined; households’ real incomes rose strongly, partly reflecting earlier declines in energy prices,and consumer sentiment remains high. Business fixed investment is advancingsoftened, while the recovery in the housing sector picked up,remained slow, and export growth has reboundeddeclined. Inflation continued to run below the Committee’s longer-run objective, partly reflecting earlier declines in energy prices and decreasing prices of non-energy imports. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations have remained stable.Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Although growth in output and employment slowed during the first quarter,The Committee continues to expect that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate. The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced. Inflation is anticipated to remain near its recent low level in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of declines in energy and import prices dissipate. The Committee continues to monitor inflation developments closely.To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

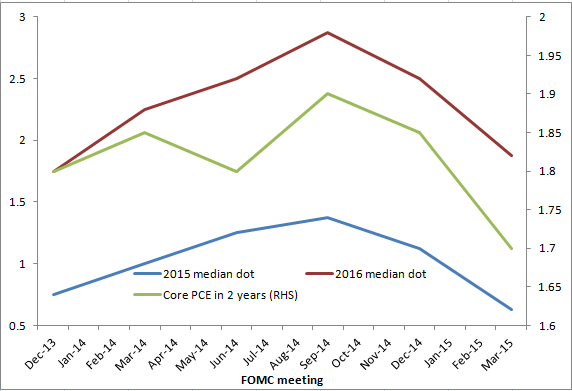

The most likely change to the economic forecasts will come in the form of a lower 2015 GDP projection. The weak Q1 (and so far somewhat disappointing bounce-back in Q2) will be enough to revise down year-end forecasts. Inflation may be revised up a little this year as well, with core PCE of around 1%. More interesting though will be whether there is any upward revision to the median core inflation projection for end-2016. It was revised down sharply in March, to 1.7% (see here for my reading of the March projections). That seems inexplicably low to me, and I wouldn’t be surprised to see some movement up (maybe a couple of tenths).

There has been a pretty good relationship between changes in the inflation outlook and the median FOMC interest rate dots. Would a move up in the inflation projection see the median dot also move up? On this occasion I doubt it.

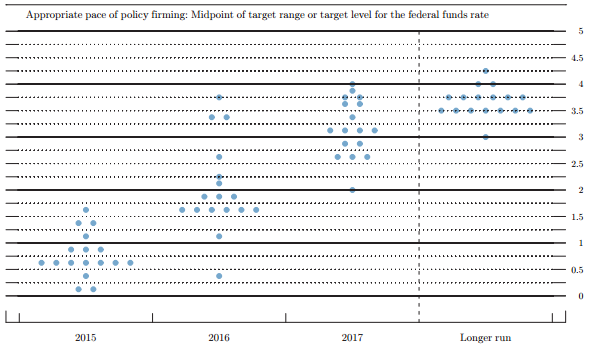

Here is the dot plot from March:

The 2015 median of 0.625% is unlikely to change, although some of the dots will move down (reflecting the later lift-off). That would still imply two hikes this year, around one more than the market currently has priced. The 2016 median is in danger of coming down from 1.875% to 1.625%, as it would require only one dot to move down, something that is quite plausible for those who envisage roughly 25bp of hikes per qtr, now starting in September. I expect 2017 and the long-run to remain unchanged.

I thought I would finish off with a few quotes from recent key Fed speakers, as they are likely to set the tone for the discussion and the press conference that follows:

Yellen (22 May)

“[The] first [headwind], is the fact that the housing crash left many households with less wealth and higher debt, weighing on consumer spending… I would score this headwind as still a concern, but one that is likely to continue to fade.”

“A second headwind has come from changes in fiscal policy to reduce budget deficits…this headwind, I hope, is mostly behind us.”

“A third headwind has been the restraining influences on the United States from the global economy…This headwind too should abate as growth in the global economy firms, supported by monetary policies that generally remain highly accommodative.”

“All of that said, the headwinds facing our economy have not fully abated, and, as such, I expect that continued growth in employment and output will be moderate over the remainder of the year and beyond.”

“Because of the substantial lags in the effects of monetary policy on the economy, we must make policy in a forward-looking manner. Delaying action to tighten monetary policy until employment and inflation are already back to our objectives would risk overheating the economy. For this reason, if the economy continues to improve as I expect, I think it will be appropriate at some point this year to take the initial step to raise the federal funds rate target and begin the process of normalizing monetary policy.”

“After we begin raising the federal funds rate, I anticipate that the pace of normalization is likely to be gradual.” [Comment: this is very similar to BoE language, something I flagged after the March press conference (here)

Fischer (26 May)

“Our mandate, like that of virtually all central banks, focuses on domestic objectives. As I have described, to meet those domestic objectives, we must recognize the effect of our actions abroad, and, by meeting those domestic objectives, we best minimize the negative spillovers we have to the global economy.”

Brainard (2 June)

“Given the softness in the data we have seen so far this year and some uncertainty about how much to attribute to temporary or statistical factors, I think there is value to watchful waiting while additional data help clarify the economy’s underlying momentum in the face of the headwinds from abroad. If continued labor market strengthening is confirmed and inflation readings continue to improve, liftoff could come before the end of the year.”

“Based on today’s picture of moderate underlying momentum in the domestic economy and the likelihood of continued crosscurrents from abroad, the process of normalizing monetary policy is likely to be gradual.”

Dudley (5 June)

“With respect to inflation, as long as growth remains strong enough to lead to further improvement in labor market conditions I am becoming more confident that inflation will move up toward the FOMC’s 2 percent objective over the medium term. The firming of inflation that I anticipate reflects my expectation that resource utilization will increase and the fact that some of the factors that have pulled down inflation, such as lower oil and gas prices and a firmer dollar, have already stabilized or partially reversed. ”

“I still think it is likely that conditions will be appropriate to begin monetary policy normalization later this year.”

“Most likely, this [hiking cycle] will be a shallow, upward path. Because of the persistent headwinds associated with the recent financial crisis, the level of real short-term interest rates consistent with a neutral monetary policy seems considerably lower now than in the past.”

“if financial conditions tighten sharply, then we are likely to proceed more slowly. In contrast, if financial conditions were not to tighten at all or only very little, then—assuming the economic outlook hadn’t changed significantly—we would likely have to move more quickly.”