Over the weekend the PBOC reduced the Reserve Ratio Requirement (RRR) for banks by more than most analysts had expected. For those unfamiliar, RRR are the fraction of bank deposits that must be deposited with the central bank; in this case the PBOC. RRR’s can be used as a monetary policy leaver, as increasing (reducing) them reduces (increases) liquidity in the banking system, increases (reduces) the cost of banking and may in turn reduce (increase) money and credit growth.

The PBOC are relatively active users of this policy lever (unlike, say, most developed economies), having raised requirements fairly sharply following the massive stimulus of 2008/09, and then gradually reducing them again as growth has slowed, notably twice this year. The cut in RRR’s over the weekend is estimated to inject around 1.3tr yuan into the banking system. Some are arguing that this is, in part, to offset recent capital outflows which are reducing the growth of the money supply (as the PBOC is intervening less).

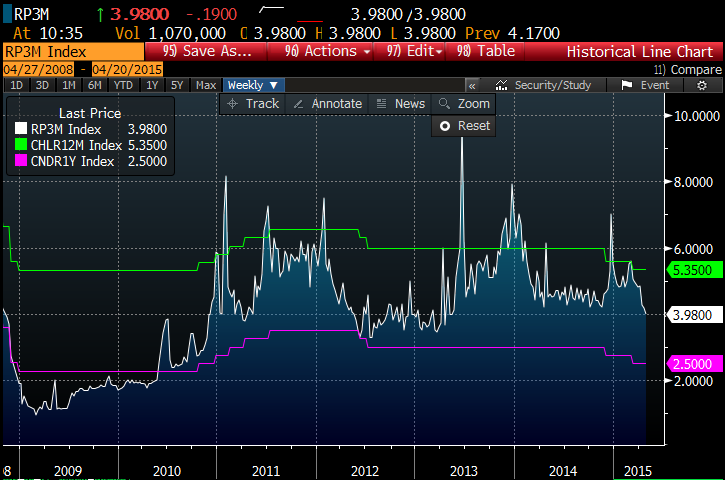

One place where RRR changes show up fairly quickly is in Chinese interbank rates, which fell fairly sharply (white line below) on the announcement, and are now around the bottom of their range for the past few years (although well above their 2009 lows). The green line below is the official policy rate (lending rate) and the purple line is the benchmark deposit rate:

But RRR’s are just one of many policy levers used by the PBOC. They list the following instruments for monetary policy: “reserve requirement ratio, central bank base interest rate, rediscounting, central bank lending, open market operation and other policy instruments specified by the State Council”.

As the PBOC controls not only the official policy rate, but also the retail deposit rate (controls on lending rates were eased last year), as well as conducting open market operations and direct lending operations to not only banks, but also corporates, you start to see how they operate a very centralised system for managing monetary policy. While they are going down the path of liberalising that system, to something closer to a western approach, there are many leaps still to be made (not least the freeing up of the capital account). And as can be seen from the chart above, there have been instances when the PBOC has lost control of domestic money markets, notably in the summer of 2013 when interbank rates soared as liquidity dried up. Some thought that was the PBOC sending a tough message to the banks – it looked to me more like a policy cock-up that was fairly quickly corrected.

Macroprudential policy

In a further attempt to target their policy actions, the PBOC also applies the traditional monetary policy instruments in a way that many would consider to be akin to macroprudential policy. Eg since 2011 RRR have not been applied uniformly across the banking system, but are applied specifically to bank types. The banks are split into small (local lenders, mainly to SMEs and agriculture), medium (regional banks, who are important property lenders) and large (the 4 state-owned mega-banks). In this latest round of RRR cuts, the small banks saw their requirements cut by an additional 100bp. Furthermore, the PBOC applies specific RRRs to certain banks, such as the “policy” banks like the Agricultural Development Bank, which got a 300bp cut this time. As a result, the Agricultural Development Bank’s RRR is now just 10.5%, compared to 18.5% for the large banks. These targeted cuts are designed to direct liquidity at those areas where the PBOC/government thinks more support is needed (as now) or where financial stability risks may be arising (as in 2010).

As I have already mentioned, the current policy easing follows an unprecedented credit and property boom in China that followed the 2009 fiscal stimulus. In order to try to contain the systemic risks associated with that boom, the Chinese authorities (led by the PBOC) enacted a range of other macroprudential policies, many of which are now either being considered or tried by advanced economies (such as New Zealand, Sweden, Canada, Switzerland and before all of them, Hong Kong). An IMF paper looks at these in more detail (here). The table below summarises the tools used:

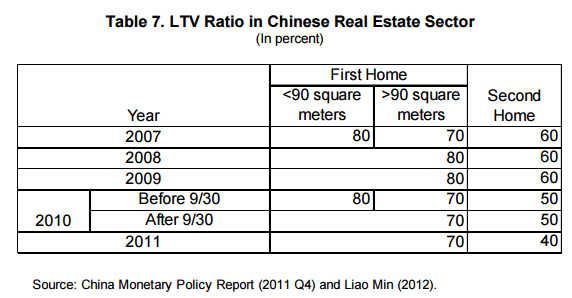

The first on the list is what I have just discussed. But the second – dynamic LTV requirements – has also been actively used by the PBOC. The table below shows the maximum loan-to-value allowable on first and second homes up to 2011. Ie there was a progressive tightening of these requirements through to 2011.

However, with the housing market cooling and house prices falling in most regions, the PBOC announced a relaxation in LTV requirements in March, increasing the maximum LTV on first homes to 80% and on second homes to 60%.

The PBOC introduced a capital conservation buffer in 2010, which alongside a new systemic capital buffer, raised the minimum capital adequacy ratio to 11.5 percent from 8 percent for large banks. In addition the provision coverage ratio was raised from 100 percent to 150 percent, and provisions were required to cover the higher of 150 percent of NPLs or 2.5 percent of total loans (although NPLs are thought to be massively under-reported).

Apart from the IMF paper, I’ve not come across any studies that look in depth at how effective these measures have been in China. But it may be difficult to get a good read-across to developed economies given the very different financial and capital market structures. Indeed, you could argue that China needed to pursue these macroprudential policies more aggressively than developed economies because of the magnitude of imbalances, and the difficulty of getting “standard” monetary transimssion mechanisms to work (as the market is so regulated). When coupled with the “one-way bet” on steady RMB appreciation, the flood of capital going into China in recent years needed to be managed. If that flood is now slowing, or worse, reversing will the authorities be able to use these policies to avoid a credit crunch?

Trading implications

As ever, it is hard to trade China macro directly. I am not close enough to the regulatory changes that have impacted the local equity market. It has clearly soared, but I just don’t know enough about it to risk trading it. If the PBOC are going to be active on the monetary and macroprudential policy front, as they appear to be, then the need for the RMB to be used as an explicit policy easing tool is reduced. But that doesn’t mean the steady appreciation trend is likely to make a comeback. So as usual, I am left trying to figure out if the structural slowing in China growth is going to turn into a more serious cyclical slowdown that could even see a severe credit crunch and serious financial instability.

I remain of the view that China will able to manage the slowdown, and prevent a severe credit crunch, even if it means that there is a series of bank bailouts. There is little doubt that the slowdown in construction (and manufacturing) has impacted a range of commodity prices (iron ore standing out as particularly impacted). That will continue to weigh on commodity exporters such as Australia. A good reason to stay short AUD.

FYI: https://youtu.be/C2SStFt-k_A?t=4s

LikeLike

Thanks for the link

LikeLike